In Portugal, unlike other countries now experiencing economic difficulties in the Eurozone - Spain, Greece and Ireland-, anemic economic growth was all too evident before the financial crisis of 2007-08. Accession to the Euro club brought a significant reduction in interest rates in those countries that had maintained historically high interest rates, which triggered real estate bubbles - Ireland and Spain, and public overspending - Greece, allowing these countries to maintain rates of economic growth above the European average. In Portugal, who suffered not only a mild housing bubble but also from government overspending, growth was much weaker than the group mentioned above and more in line with countries that have had lacklustre performances in the European context: Germany; Italy. (See chart below)

What’s the reason for the low growth relatively to other countries that are now in the same situation? To put another way, what’s the cause that differentiated Portugal from the other countries before the crisis of 2007-08, and how it faded since? Some recent papers and articles attempt to explain the causes of this relative weak performance, but although some of the causes advanced can in part explain the weak growth in Portugal, they do not fully explain the low growth relatively to the group mentioned above because many of the issues were also present in the other countries before the crisis.

What’s the reason for the low growth relatively to other countries that are now in the same situation? To put another way, what’s the cause that differentiated Portugal from the other countries before the crisis of 2007-08, and how it faded since? Some recent papers and articles attempt to explain the causes of this relative weak performance, but although some of the causes advanced can in part explain the weak growth in Portugal, they do not fully explain the low growth relatively to the group mentioned above because many of the issues were also present in the other countries before the crisis.

Long term economic growth can be split into labor force growth and productivity growth. Invariably, the main cause cited for the Portuguese low growth has been productivity growth, or the lack of it, but although this certainly has been a problem in the last decade, not so much before, it hardly appears enough to explain the relative week performance. The differences in productivity gains don't seem big enough to justify the differences in GDP growth, even in the cases of Ireland and Greece, countries where productivity growth was higher than Portugal; but certainly this is true for Spain as its productivity growth was smaller than Portugal, as can be seen in the chart below. In the last decade, productivity growth in Portugal was threefold that of Spain but its growth was less than half.

As such, we can safely conclude, that productivity on its own cannot explain the differences in economic growth between Portugal and the other group of countries. On the other hand, the stagnation and decline of the working-age population can not only explain the weak economic growth that afflicted Portugal, but also the GDP growth differences between several countries in the Eurozone before the crises.

As explained in the previous post, between 2003 and 2008, working-age population growth in Portugal was negligible and as such the “workforce effect” - contribution of labor force growth to GDP growth - was non-existent, as can be seen in the chart above. Starting in 2008, working-age population growth became negative and thus the “workforce effect” began to act as drag on the economy. To maintain a healthy economic growth Portugal had to gradually increase its productivity growth, and/or alternatively increase its labor participation rates - to compensate for the declining workforce-, but this is not easily attainable, as such, trend growth will surely steadily fall. Therefore, when the labor force starts to stagnate or decline, economic growth stalls. This explains the weak economic growth in several European countries in the last decade. In particular, it explains why Portugal and Spain had very different economic performances before the 2007-08 financial crises and how this began to converge after this.

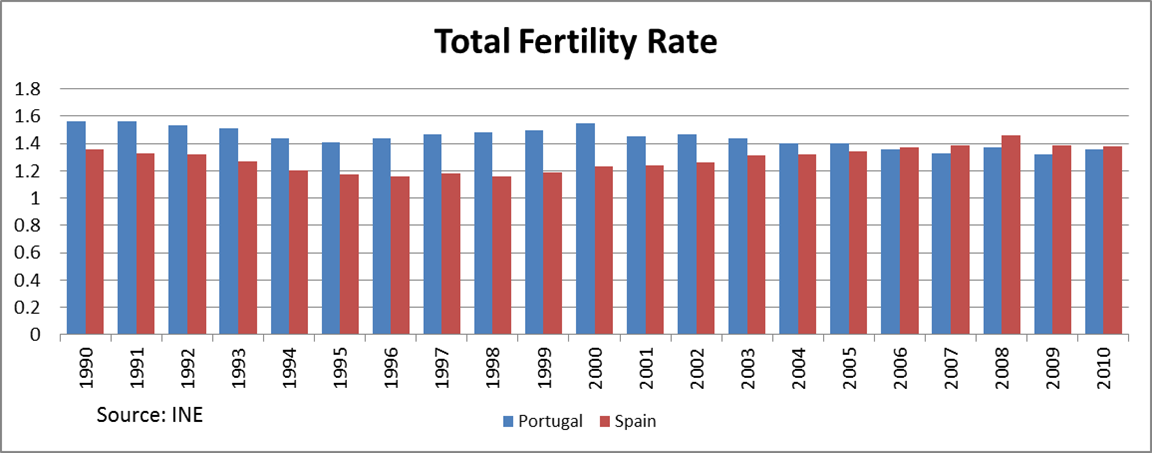

Population change is comprised of natural growth, the difference between births and deaths, and net migration, the difference between immigration and emigration. Natural growth, both for Portugal and Spain, had been barely edging positive in the turn of the century since in both countries the total fertility rate fell below replacement level in the early 80’s. In Portugal, natural growth turned negative in 2007, the year that for the first time there were more deaths than births. On the contrary, Spain experienced a slight recover of its natural growth in recent years, as a result of an increase in its total fertility rate, as can be seen in the chart below, although this is due almost exclusively to foreigners, who have a higher fertility rate than the native-born.

As a result, both in Portugal and Spain, population growth in the last decades depended almost exclusively on having a positive net migration, and this resulted in a large influx of immigrants. But while in Portugal this growth began to slow down since 2002, in Spain immigration exploded until 2007, as can be seen in the chart below. "No modern country on Earth experienced such a massive increase in its immigrant population as Spain. In 1990, one in 50 people in Spain was an immigrant. Today, it's one in seven."

Portugal not only received fewer emigrants from 2000 onwards, but also witnesses a massive exodus of its nationals. As Edward Hugh pointed out, the entry in the European Union was accompanied by steady emigration flows, which clearly sets Portugal apart from the other countries, Spain in particular (see map on page 11), and resembles more the path that would be later trodden by Eastern Europeans countries when of their accession to the European Union. Consequently, and according to the Instituto Nacional de Estatística (Statistics Portugal), during the inter-census period, the resident population of Portugal increased by only 1.9% while in Spain, the increase was 12.9%. (Chart below)

With the accession to the European Monetary System and later the Euro, interest rates declined significantly for both Portugal and Spain and as a result the two increased their debt levels. According to the McKinsey report, Debt and deleveraging (see page 14), in the second quarter of 2011 Portugal and Spain had total debt of 356 and 363 (as % of GDP), respectively. The consequence of cheap and easy credit was to create a housing bubble, both in Portugal and in Spain, but while the Portuguese began to deflate in 2002, the Spanish continued to inflate until 2008. This outcome was the result of the substantial increase in Spain’s population as a result of immigration, many of them Portuguese, while the increase in immigration in Portugal was just enough to replace the ones who were leaving. This population growth allowed the housing bubble to continue for much longer in Spain, while in Portugal there were no longer enough people to buy the excess homes being built, and so prices didn't skyrocket; but the housing units were built regardless. As such, rather than a classical bubble with inflated house prices, in Portugal, it was more a case of oversupply, given that 800,000 homes were built in the last decade while the population only grew by 200,000. On the contrary, in Spain, in addition to the excess construction, prices went through the roof, with immigration having a great influence on both. It is estimated that the immigration inflow increased house prices by about 52% and was responsible for 37% of the total construction of new housing units between 1998 and 2008. From 2002 until the 2007-08 financial crises, the growth of the Portuguese economy began to be more in line with the growth of economies where the labor force was stagnant or declining, namely Italy and Germany, as can be seen in the chart below.

The chart above is easier to understand if we group countries into two groups: countries with weak economic growth – Portugal, Germany and Italy-, and countries with more healthy growth - Spain, Ireland and Greece. With the exception of Greece, countries with sound economic growth before the recession were also the countries with higher labor force growth in the same period, as shown in the graph below. By contrast, in countries where economic growth was weaker, the labor force growth was also more moderate or even negative, as in Germany. (Chart below)

However, the dynamics changed completely with the onset of the 2007-08 recession. In Spain, where working-age population growth depended exclusively on immigration, the rates of labor growth collapsed, only matched by the plunge of its GDP growth, and its workforce has actually started to shrink. In Ireland, despite a more abrupt fall, growth nonetheless remained positive, this was due to the fact that its population growth did not depend only on net migration but had an important natural component as well. In fact, Ireland has the highest fertility rate amongst European countries and therefore, unless immigration returns to numbers only seen in previous centuries, growth of its working-age population should stabilize in positive territory, although at a level well below the pre-crisis.

In Portugal and Greece, even before the 2007-08 recession, the labor force growth already showed clear signs of a slowdown, as growth came to a standstill in 2005, and despite a slight recovery after, more pronounced in Greece than Portugal, working-age population went into decline with the onset of the recession. Italy, which had reversed the decline of its working-age population initiated in the 90’s, appears once again to slide back into negative territory. On the other hand, in Germany, the workforce began to grow for the first time since 1998 due to an increase in immigration, many of them Portuguese, Spanish, Italian and Greek.

As explained by Daniel Gros, when comparing economic growth performance between countries with very different rates of population growth, the best indicator is undoubtedly GDP per Working Age Person (GDP/WAP).

Hence, if we compare the per working-age person GDP growth between the various countries in the last decade, as such taking working-age population growth out of the equation, it can be said that neither the growth of Spain and Ireland was so spectacular, nor the growth of Portugal, Germany and Italy fared so badly in comparison. In fact, only Greece seems to have had a spectacular growth, which would be in line with its productivity growth before the recession, but Greece’s population statistics might be underestimated, as Greece has not only a large population of illegal immigrants but some weakness in data collection have also been highlighted. Anyway, its growth was probably due to other unrepeatable factors, such as the Olympic Games. It also should be highlighted the economic growth achieved by Germany despite the decline of its workforce, proving that growth is possible with a declining population.

Despite some regional variations as a result of internal migrations, the reality is that working-age population in the Eurozone as a whole has initiate a long downward trend that will have major repercussions in terms of its economic growth, as explained in the previous post, and therefore, we can also conclude that Europe suffers from a "shortage of Japanese" as shown in the graph below.

As such we cannot fully comprehend the situation that Portugal, Spain and Greece face at the moment without looking into their adverse demographics. This already exerted an disproportional role in the last decade, namely in Spain, whose working-age population growth goes a long way explaining its outstanding economic growth, while for Portugal the contrary it’s true, as the lack of population growth made its economy lose steam as it joined the Euro. More worryingly tough, is that working-age population in Europe as a whole has started a long, perhaps irreversible, path of decline that will act as a drag on its economic growth, making the economic recovery for these countries even more difficult.

.png&filetimestamp=20130129121040){kind=link}